Imagine this: you buy a house with zero downpayment, and on top of that, you walk away with a massive lump sum of cash in your pocket. Sounds like the ultimate financial hack, right?

In the real estate world, this is known as a “Cash-Out” or “Cashback” scheme. As a property agent with years of experience under my belt, I’ve noticed that this trend hasn’t faded at all. In fact, it has become highly “professionalized.” Some first-time homebuyers have even turned the ability to “cash out” into their primary criteria for choosing a property.

But before you jump onto this bandwagon, let’s strip away the marketing hype. We won’t talk about morals or whether this is “right or wrong.” Instead, let’s break down the underlying mechanics, look at a couple of realistic case studies, and explore what your ultimate exit strategy looks like.

The Mechanics: How Does a “Cash-Out” Actually Work?

Before “cash-out” deals became a trendy marketing hook, property owners typically extracted cash through a legitimate process called Refinancing.

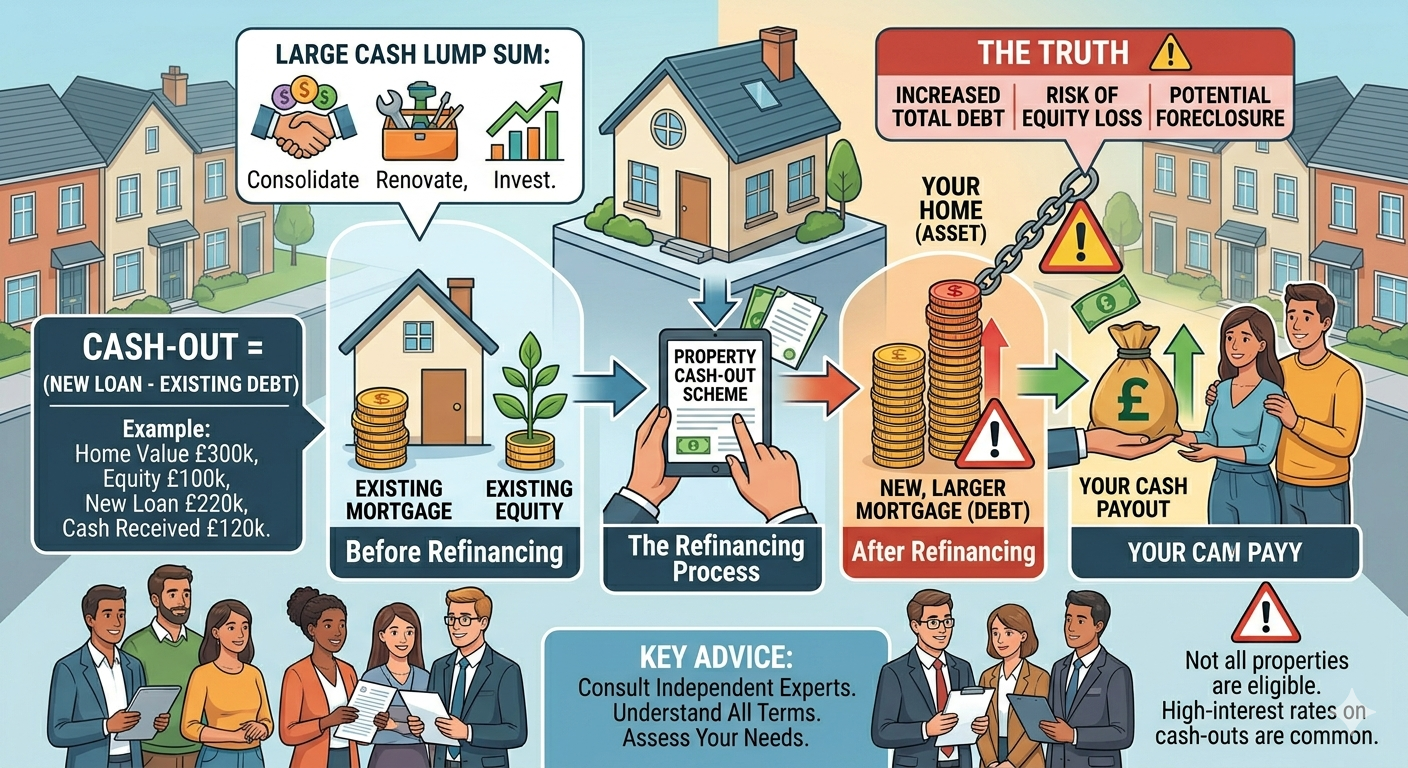

1. The Legitimate Way: Refinancing (Equity Extraction)

This is a standard, fully legal financial move based on genuine capital appreciation.

- Example: You bought a house 20 years ago for RM400,000. Today, the market value has risen to RM800,000.

- By refinancing your mortgage against the new valuation, you unlock the equity built up in your asset. This is a reward for your asset’s organic growth.

2. The Trendy Way: The “Mark-Up” Scheme

The modern “cash-out” often relies on inflating the purchase price on paper. Here is how the math works:

- A seller is desperate to let go of a property for RM450,000.

- However, a bank valuer estimates the market value of the area can stretch up to RM650,000.

- The buyer and seller agree to write the Sale and Purchase Agreement (SPA) at the inflated price of RM650,000.

- The bank approves a 90% loan based on the SPA price, which equals RM585,000.

- After paying the seller their required RM450,000 and covering legal fees, stamp duties, and valuation costs, the buyer is left with roughly RM100,000 in cold, hard cash.

The Catch: That RM100,000 is not a profit, nor is it a bonus. It is a high-interest loan you are borrowing from your future 35-year-old self.

Why Is There Still a High Demand for Cash-Out Properties?

Buyers aren’t foolish; they know this is debt. Yet, for many, these properties serve as a desperate financial lifeline. Here are the three main reasons people seek them out:

- Debt Consolidation: Swapping high-interest debt (like 18% credit cards or 8% – 10% personal loans) for a much cheaper mortgage rate (around 4%) stretched over 35 years.

- Low-Cost Business Capital: For small business owners, getting a business loan can be incredibly difficult and expensive. A mortgage is often the cheapest, longest-term financing available on the market.

- Anxiety Over Rising Prices: Many fear that if they don’t buy a home now, they will be priced out forever. “Zero-down” with cashback schemes make entry possible for those with no savings for downpayments and legal fees.

Case Study 1: The Debt Consolidation Trap (Mr. A)

Let’s look at a simulated scenario to see how this plays out in real life.

The Profile:

- Mr. A earns RM7,000 a month.

- He has RM50,000 in credit card debt (18% interest) and a RM30,000 personal loan (8% interest).

- Total debt: RM80,000.

- His monthly debt installment is RM3,500, eating up half of his take-home pay.

The Transaction: Mr. A finds a sub-sale apartment valued at RM300,000 that allows him to cash out RM100,000.

The Outcome: He uses the RM100,000 to wipe out his credit card and personal loans. Because the mortgage rate is only 4% and spread over 35 years, his monthly debt obligation drops from RM3,500 to just RM1,800. He feels like an absolute winner.

The Hidden Danger: If Mr. A does not change his spending habits, the relief is temporary. Two years later, feeling less financial pressure, he starts swiping a new credit card and signs for a new car loan.

Now, he is burdened with a much larger mortgage plus brand-new consumer debt. In this scenario, cash-out acted merely as a financial painkiller—it masked the symptoms but didn’t cure the disease.

Case Study 2: The “Negative Equity” Illusion (Mr. B)

Now let’s talk about the aspiring “investor.”

The Profile:

- Mr. B hears about a project that offers a RM150,000 cash-out.

- He plans to use this cash to buy yet another property, collect rent, and fast-track his journey to financial freedom.

The Transaction: He buys a property marketed as “Below Market Value” (BMV). To secure the RM150,000 cash-out, his monthly mortgage installment is marked up from RM1,000 to RM2,200.

The Outcome: Because the property is located in a remote, less-developed area, the actual rental demand is weak. He can only rent it out for RM1,000 a month. This is a common reality in cash-out marketing: “Pay RM2,200 monthly, rent it out for RM1,000, and top up RM1,200 as a form of ‘forced savings’.”

Within three years, the RM150,000 cash-out he received is entirely drained by monthly top-ups, maintenance fees, and miscellaneous expenses. When he decides to sell, he realizes the actual market value of the property is only RM300,000—but because of the inflated loan, he still owes the bank RM400,000.

Mr. B is now trapped in Negative Equity. He has effectively pre-spent 15 years of future property appreciation. Until the market value catches up to his inflated loan, he cannot exit.

The Harsh Reality: Why Prime Properties Don’t Have “Mark-Up” Room

Having operated in prime areas like Cheras for years, I can tell you that high-quality, secondary market properties rarely have room for mark-ups.

The sub-sale market is open and transparent. If a seller owns a well-maintained property in a highly desirable location with strong demand, why would they voluntarily undervalue their property or collude in inflating contracts just to help a buyer cash out? They simply don’t need to.

Properties that offer massive cash-outs typically share very specific traits:

- Terrible Condition: The property requires massive capital expenditure just to be livable.

- unpopular/Remote Locations: There is zero organic buyer or tenant demand. The developer or seller must offer “cashback” as a gimmick to lure buyers.

- Valuation Bubbles: The price has been artificially pumped up through aggressive or non-standard valuation methods.

If your primary goal in buying a property is to “get cash” rather than to acquire a high-quality asset, you have strayed very far from the core principles of investing.

A Final Thought: Lifeline or Black Hole?

The rising popularity of cash-out schemes is a reflection of our collective anxiety over the rising cost of living. When times are tough, treating a house like a personal ATM seems like the only way to survive.

But let’s step back and look at the macro picture: If a country’s real estate market is no longer driven by location, amenities, and quality of living—but is instead kept alive by lending extra money to buyers just to sustain transaction volume—how much longer can that market run?

I am not here to completely condemn cash-out properties. Everyone has their own financial struggles, and sometimes desperate times call for desperate measures. But I want you to look at the numbers honestly.

Let’s bring this to the comments section: If someone is already in a position where they must take on 35 years of debt just to get immediate cash, is this extra mortgage debt actually solving their financial problems? Or is it simply pulling them deeper into a black hole they can never escape?

Are we doing this to survive today, or to build actual wealth for tomorrow?

Let me know your thoughts below.

I’m Vincent Tai. Don’t forget to subscribe to my YouTube channel and like my Facebook page. See you in the next post!